This report provides a structural, architectural, and financial assessment of CBRS to evaluate whether its wafer-scale technology warrants its premium valuation.

Following its highly anticipated mid-May 2026 listing on the Nasdaq, Cerebras Systems (CBRS) has emerged as one of the most polarizing and closely watched mega-unicorns in the semiconductor sector. With its market capitalization rapidly approaching the $100 billion threshold post-IPO, the company is being framed by institutional growth capital as the ultimate challenger to NVIDIA’s dominance in large-scale AI cluster computing. This report provides a structural, architectural, and financial assessment of CBRS to evaluate whether its wafer-scale technology warrants its premium valuation.

I. Core Investment Thesis: Wafer-Scale Integration vs. "Chipped" Monopolies

Traditional AI compute architectures—exemplified by NVIDIA’s DGX systems—rely on advanced packaging (e.g., TSMC’s CoWoS) and high-speed interconnects (such as NVLink) to stitch together thousands of individual dies carved out of conventional silicon wafers. The fundamental physical limitation of this approach is the communication bottleneck: data transmission across discrete chips incurs massive latency penalties and high energy dissipation compared to on-chip communication.

Cerebras bypasses this bottleneck entirely through its proprietary Wafer-Scale Engine (WSE) technology. Instead of dicing a standard 12-inch silicon wafer into hundreds of separate chips, Cerebras manufactures a single, gargantuan processor utilizing the entire wafer surface area. Its latest-generation WSE-3 processor boasts unprecedented technical specifications:

- Transistor Count: 4.4 trillion transistors (in contrast, NVIDIA’s Blackwell B200 houses 2.08 trillion).

- AI-Optimized Cores: 900,000 fully programmable, sparse compute cores.

- On-Chip Memory: 44GB of Static RAM (SRAM), eliminating the immediate, supply-constrained dependency on external High Bandwidth Memory (HBM).

- Memory Bandwidth: 21 PB/s (petabytes per second), orders of magnitude faster than off-chip memory sub-systems.

Architectural Alpha: By consolidating the equivalent compute of hundreds of traditional GPUs into a single piece of contiguous silicon, Cerebras achieves near-instantaneous on-wafer data routing. For training Large Language Models (LLMs) with hundreds of billions of parameters, this eliminates the need for complex distributed tensor-parallel programming models, allowing developers to treat a massive cluster like a single, easily programmable GPU.

II. Commercialization, Monetization, and Financial Assessment

Cerebras generates revenue through two primary business vectors: the direct sale of its computing systems (the CS-3 server built around the WSE-3) and a consumption-based cloud model via the Cerebras AI Model Studio, which rents out massive dedicated compute clusters. The company’s commercial engine has witnessed explosive scaling between 2024 and 2026.

Cerebras CS-3 computing cluster, purpose-built

for supercomputing and LLM training. Source: Cerebras

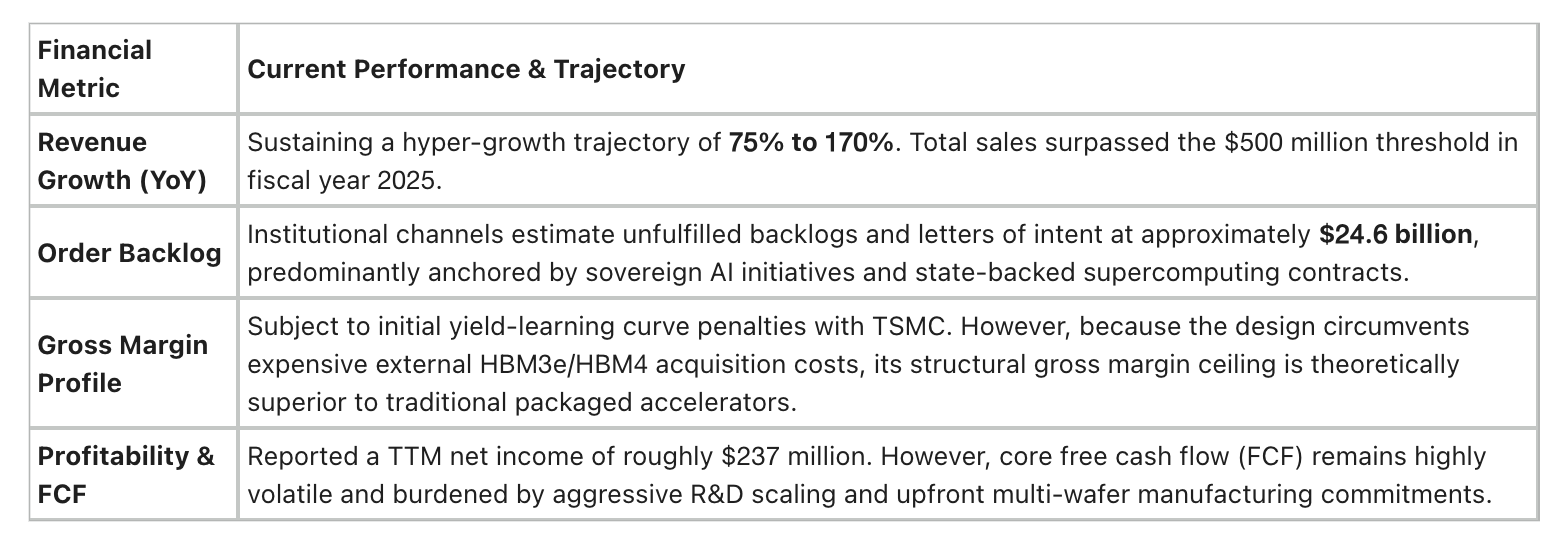

Key Financial Characteristics (As of Q2 2026)

III. Competitive Landscape: Assessing the NVDA Imperium

To determine if CBRS can structurally capture market share, its strategic advantages must be weighed against formidable ecosystem barriers.

Strategic Advantages (The Bull Case)

- Single-Node Compute Velocity: In ultra-large LLM inference and specific single-step training sequences, the absolute latency reduction of the WSE-3 enables tokens-per-second performance metrics that outperform GPU clusters by multiples.

- Insulation from HBM Shortages: By utilizing massive ultra-fast on-chip SRAM, Cerebras completely bypasses the global structural supply deficit of HBM allocation, a critical vulnerability for traditional hyperscale suppliers.

- Institutional Growth Support: Strategic capital reallocations—such as Cathie Wood’s ARK Invest rotating capital heavily into CBRS post-IPO—highlight a growing institutional mandate to diversify risk away from a pure NVIDIA monoculture.

Structural Risks (The Bear Case)

- Extreme Customer Concentration: A massive portion of historical and pipeline revenue is tied directly to the United Arab Emirates’ AI champion, G42. This single-source concentration leaves Cerebras heavily exposed to shifts in geopolitical alignment, export control restrictions, and federal regulatory oversight from Washington.

- TSMC Single-Point Vulnerability: Cultivating a defect-tolerant 12-inch monolithic wafer-scale architecture requires deep co-engineering that only TSMC can execute. Cerebras remains entirely dependent on TSMC's allocation priorities.

- The CUDA Software Moat: While Cerebras provides robust software compilation stacks that natively interface with PyTorch, breaking NVIDIA’s decade-long CUDA software ecosystem dominance remains an uphill battle for broader enterprise SaaS and general-purpose commercial cloud adoption.

IV. Valuation Judgments and Portfolio Allocation Strategy

Following its immediate post-IPO run, Cerebras’ valuation trades at highly demanding multiples, reflecting an intense divergence between momentum-driven retail investors and disciplined institutional allocators. Trailing Price-to-Sales (P/S) multiples hovering above 100x reflect an assumption of near-flawless execution.

Furthermore, a critical nuance lies in its corporate structure: CBRS's lock-up period expiration terms are tied explicitly to specific operational and financial milestones rather than a rigid calendar date. This creates an environment where abrupt tranches of early venture and insider equity could enter the public float upon upcoming earnings releases, triggering sudden liquidity events.

Investment Conclusion:

Cerebras Systems represents a high-beta, technically pure-play vehicle capturing a profound structural shift in AI processor architecture. However, at its current rich valuation, chasing the momentum carries significant downside risk. The optimal portfolio strategy is to treat CBRS as a strategic tactical overlay or a structural hedge against NVIDIA (NVDA) positions. Institutional allocators should wait for valuation compression toward historical technology-disruptor P/S averages and monitor upcoming quarterly filings for revenue diversification beyond G42 before executing aggressive accumulation.